Completing tax returns can be a nightmare for many of us. However, completing Form

12BB is not as scary as it may seem. So, let's get down to it!

Just follow these

instructions to understand and complete the complete form for maximum tax return.

Now let's talk about each of them in detail:

I. Personal Details :

This is the first section of Form 12BB, you need to mention your :

- Full Name

- Address

- Permanent Account Number

- Financial year (Current Financial Year is F.Y. 2017-18)

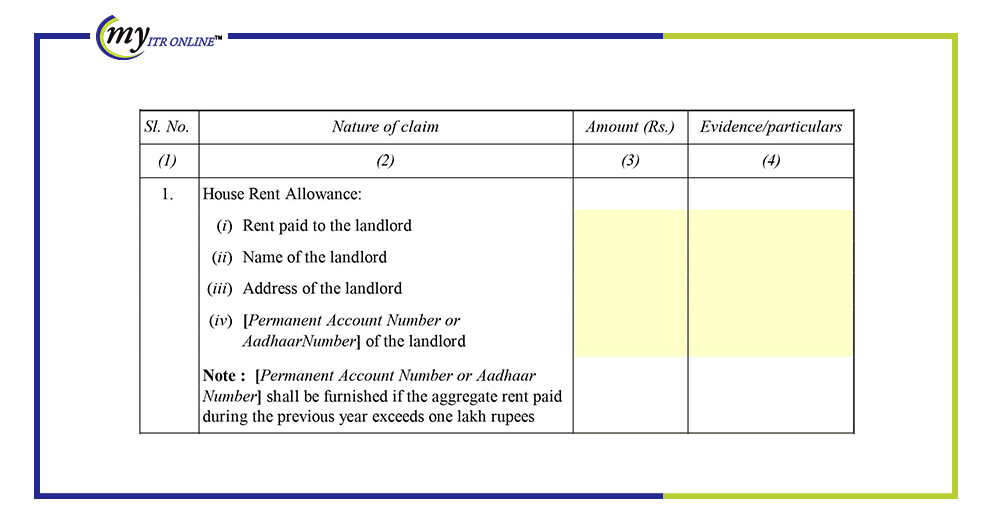

II. HRA(House Rent Allowance) :

For claiming HRA tax exemption, you need to submit the following details to your

employer -

- Amount of Rent paid

- Name of your landlord

- Address of your landlord

- PAN No of your landlord in case the total amount of rent paid during the year

exceeds Rs.1 lakh.

In Addition, you also need to submit the proof for claiming HRA tax exemption .

1. Evidence/Proof for claiming House Rent Allowance tax exemption:

The proof for claiming HRA tax exemption is the monthly rent receipts. In many

organizations, employers also asks for the rent agreement for allowing HRA tax

exemption.

2. Amount of tax saving on House Rent Allowance(HRA):

This is the best tax saving avenue.Calculate your HRA tax exemption with our free HRA exemption

calculator tool.

Read our complete guide on rent

receipts to know in detail how you can claim HRA tax exemption to save

maximum tax

3. Things to remember when claiming HRA tax exemption :

- You can claim HRA tax exemption only when HRA is a part of your CTC.

- In case, HRA is not a part of your CTC and you are living in a rented house you

can claim tax benefit under section 80GG.

- A rent receipt is required only when your monthly rent exceeds Rs. 3,000.

- You can’t claim HRA if you are living in your own house.

- If you are paying rent to your parents, then ask them to show it as their income

at the time of filing their Income Tax Return.

- Never submit fake rent receipts, this might land you in big trouble with the

income tax authorities.

- Even if your employer does not ask for a rent agreement, it is advisable to have

a formal rent agreement printed on Rs. 500 stamp paper or as per the rate

prevailing in your state for records.

III. LTA(Leave Travel Concession/Allowance):

This allowance is one and the only allowance that helps save tax only when you take a

holiday.

1. Evidence/Proof for claiming LTA tax exemption:

To claim LTA, employees need to submit travel bills like boarding passes, flight

tickets, invoice of a travel agent, boarding pass, etc. to the employer.

2. Amount of tax saving on LTA :

This tax exemption is allowed only on actual travel costs to the extent specified in

CTC. The fare is exempt as per the following conditions:

| Travel Mode |

Exempt Amount |

| Air |

Airfare of economy class in the National Carrier by the shortest

route or the amount spent, whichever is less |

| Rail |

Air-conditioned first-class rail fare by the shortest route or the

amount spent, whichever is less |

| Bus |

First Class or deluxe class fare by the shortest route or the amount

spent, whichever is less |

| Unrecognized public transport system |

Air-conditioned first-class rail fare by shortest route or the

amount spent, whichever is less |

3. Things to remember when claiming LTA tax exemption :

- You can claim LTA only when it is a part of your CTC.

- You can claim LTA for yourself, your spouse, children, dependent parents, and

dependent brother and sister.

- It can be claimed twice in a block of four years. The current block is

2021-2022.

- If you have claimed only 1 LTA in the previous block of 4 years, you can carry

forward and utilize the 2nd LTA but have to claim it in the first year itself of

the next block.

- It is allowed for domestic travels and not for international travels.

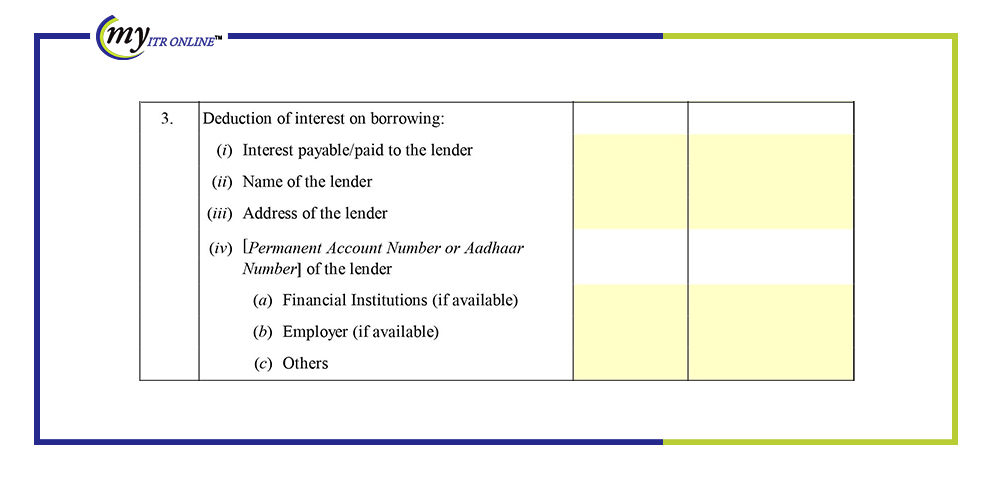

IV. Deduction of Interest on Borrowing :

Deduction of interest on borrowings on a home loan is allowed under section 24 of the

income tax laws. You can claim a deduction for interest on your home loan taken for

construction, reconstruction, repair, purchase, or renovation.

The information needs to be filled in the Form 12BB are:

- Interest Payable/paid to the lender during the financial year.

- Name of the lender from whom the loan is taken.

- Address of the lender.

- PAN of the lender: Financial Institutions/Employer/Others, from whomever the

loan is taken.

1. Evidence/Proof for Claiming tax exemption for interest on borrowing:

Documents required to claim deduction u/s 24B on interest payment of home loan are:

- Statement / Certificate stating total EMI paid along with Interest and Principal

components.

- Possession/construction completion certificate.

- Self-declaration from employees whether the house is self-occupied or let out.

2. Amount of saving on Home Loan :

a. Tax benefits on payment of interest :

If you are paying interest on a home loan, then the quantum of deduction will depend

on the type of house property. Let’s discuss the same in detail.

Tip: Claiming deduction on interest payment shall result in a loss under head

house property. This loss can be adjusted against income from other heads in the

current year subject to the limit of Rs. 2 lakh.

I. Tax benefit in case you have the self-occupied property (SOP):

The maximum interest of Rs. 2, 00, 000 is allowable in case a loan is taken for the

purchase or construction of your house. Such benefit shall be reduced to Rs. 30, 000

in case a loan is taken for repair/ reconstruction. Further, construction or

purchase must be completed within 5 years from the end of F.Y. in which loan is

taken.

II. Tax benefits in case you have rented out(let-out) the property (LOP) :

The entire interest amount that you pay towards the loan is available as a deduction

in the case of the rented property. Such amount shall be deducted from the rental

income for the year.

Note : However, from 1 April 2017 onwards i.e. F.Y. 2017-18, the

maximum tax exemption of Rs.200,000/- can be taken for all types of

houses(let-out/self-occupied). In case, you have paid more than Rs.2,00,000 as

interest on a home loan taken for construction/purchase, then the remaining

amount shall be allowed to be carried forward for set-off in subsequent years.

b. Tax benefits on repayment of Principal Amount :

In both cases, whether there is self-occupied property or rented property, principal

amount repayment is eligible to be claimed under Sec 80C of the income tax act. A

maximum of Rs. 1.5 lakh can be claimed under Sec. 80C for the principal amount.

(Max. The limit of claiming all deductions under 80c is 1.5 lakh. So, plan

accordingly.)

3. Things to remember when claiming Interest on Home Loan tax exemption :

- In case, you have taken a home loan jointly then you can claim the benefit of

the interest deduction proportionately.

- If you have taken a home loan from a lender other than the bank i.e. your

friends, relatives, or any money lender the interest payment can be claimed as a

deduction under section 24. Provided you take a certificate of interest from the

person to whom you had paid interest.

- Where a loan is taken from your friends, relatives, or any money lender i.e.

other than banks the repayment of principal is not eligible for deduction under

section 80C.

This part of the form may take more time to finish if you are claiming maximum tax

benefits. If you do not have any deductions to make, you can then move on to the

last section.

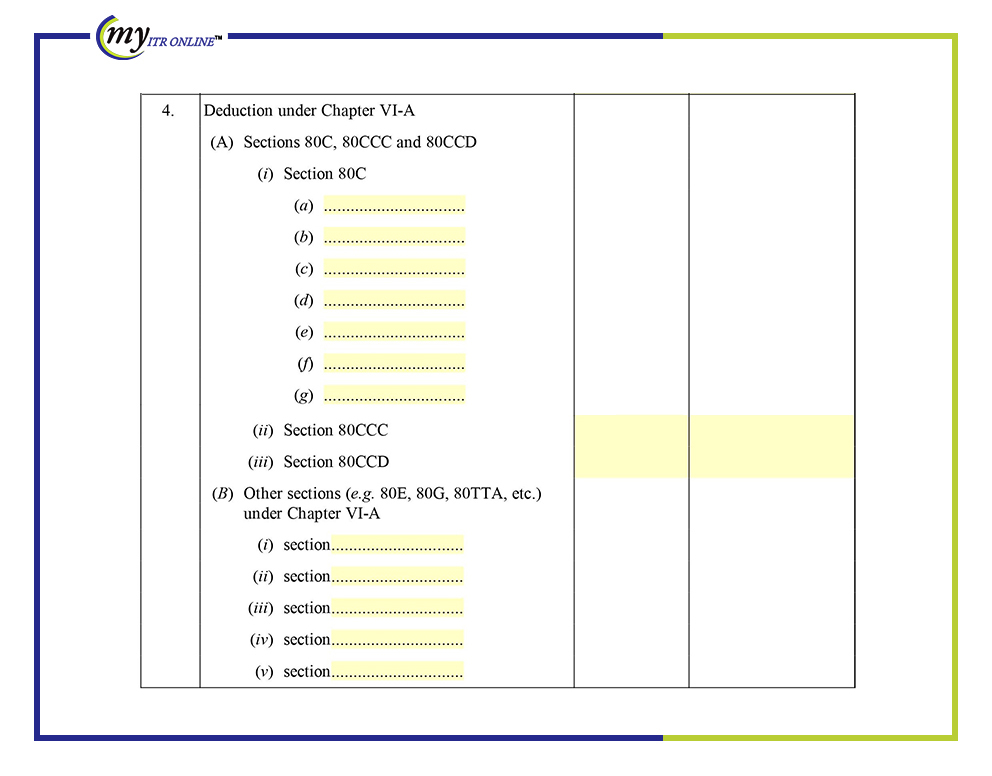

V. Deductions under Chapter VI-A

Chapter VI-A covers income tax deduction under various sections like 80C, 80D

(Medical insurance) 80G (Donation), etc. To claim the deduction, evidence of

investment made or expenditure incurred is required. You might be wondering what

kind of proofs are required to submit to claim these deductions. Don’t Worry, we are

here to help you.

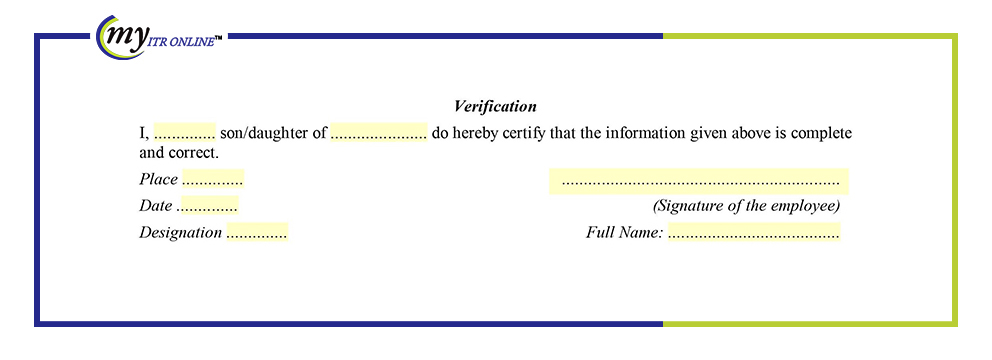

VI. Verification

The last section of Form 12BB is the “verification” of the information submitted in

Form 12BB. You need to just enter your name along with the name of your

father/mother and the place(a city in which you are filling the form) and the date

of filing the form and then sign the form.

Done!

Easy isn’t it!

“In order to avoid tax deduction altogether, you’ll have to have no tax liability

this year “